Fbr Circular 07 2026 Section 7F 236C Exemption

Builders Can Avoid 236C Tax – FBR Circular 07 (2026) Explained

Introduction

FBR Circular 07 (2026) has clarified an important issue for builders and developers in Pakistan regarding Section 236C (advance tax on sale of property) and Section 7F (special tax regime).

Understanding Section 7F

Section 7F provides a special tax regime for builders and developers where:

Tax is calculated on a fixed or prescribed basis

Income is treated as business income

Capital gains tax (CGT) does not apply in the usual way

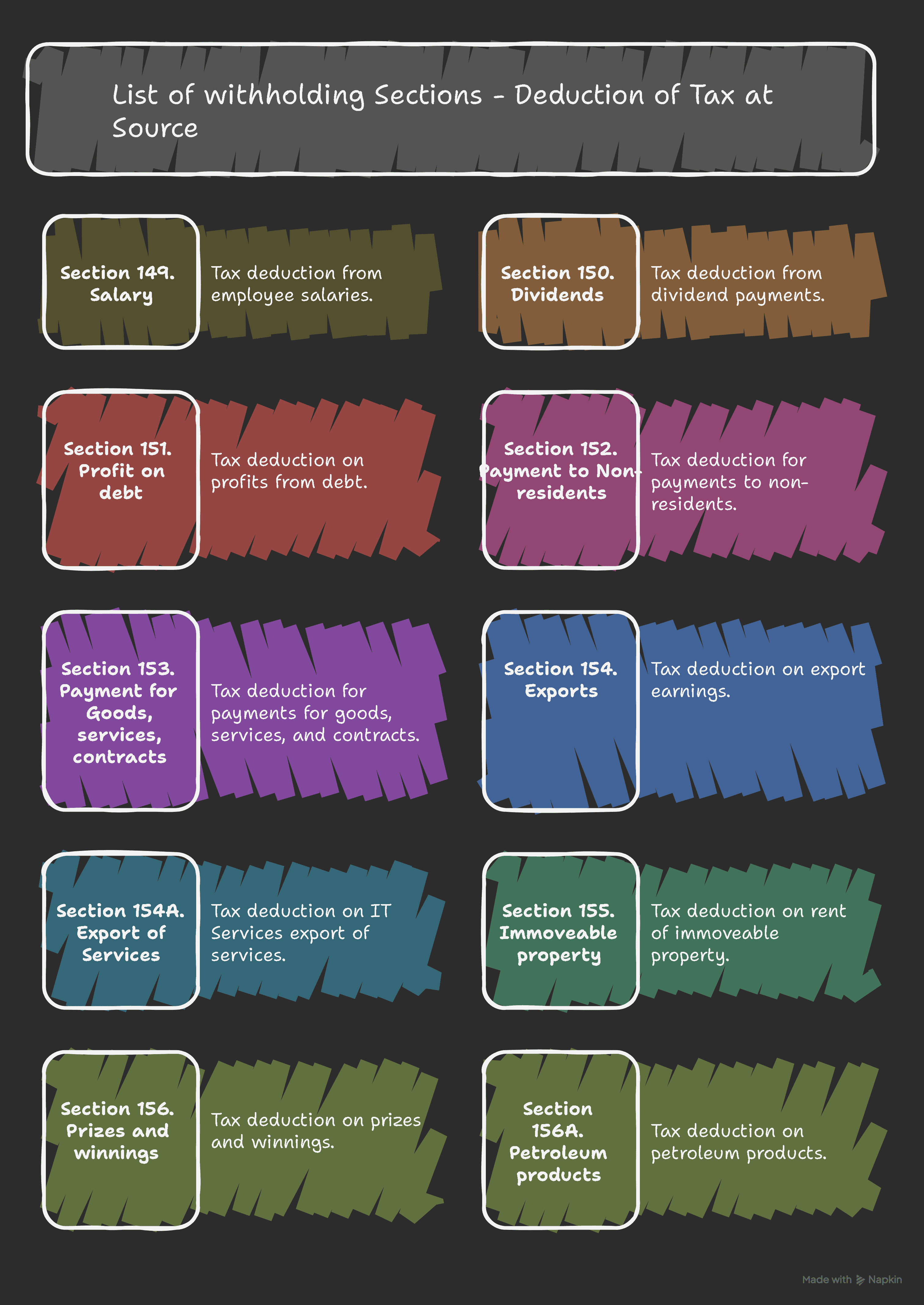

What is Section 236C?

Section 236C is advance tax collected on sale of immovable property. Normally:

It is adjustable against capital gains tax

It acts as advance or minimum tax

The Core Issue

Builders under Section 7F:

Do not pay tax under capital gains

Are already taxed under a special business regime

So: 236C becomes non-adjustable and turns into an extra burden.

FBR Clarification – Circular 07 (2026)

FBR clarified that builders and developers under Section 7F can apply for exemption from Section 236C.

Why?

Because their income is already taxed under a special regime (7F), so applying 236C creates unnecessary duplication.

How to Claim Exemption

Apply under Section 159

Submit request to Commissioner Inland Revenue (CIR)

Show that you fall under Section 7F and 236C is not adjustable

Role of Commissioner

Reviews case

Grants or rejects exemption

Exemption is not automatic

Practical Impact

Better cash flow

No unnecessary tax deduction

Improved financial planning

Key Takeaway

Builders under Section 7F should apply for exemption to avoid extra tax burden.

Conclusion

This circular removes confusion and ensures fair taxation. It helps builders avoid unnecessary withholding and manage cash flow better.

One-Line Summary

Builders under Section 7F can apply for exemption from Section 236C because their income is already taxed under a special regime.